Buying a House Used to Fit on Two Pages. Now It Takes a Filing Cabinet.

The Deal That Happened Over Coffee

Somewhere in the late 1950s, a man named Robert sat down at a kitchen table with his neighbor, a local real estate agent he'd known for years, and a banker who'd financed half the houses on the block. By the time the coffee was cold, they'd agreed on a price for a three-bedroom house on Elm Street. The deed was straightforward. The mortgage terms fit on a single page. Everybody shook hands.

Robert moved in three weeks later.

That transaction would be unrecognizable today. The modern American home purchase involves title searches, title insurance, escrow accounts, home inspection contingencies, appraisal contingencies, financing contingencies, lead paint disclosures, flood zone disclosures, HOA disclosure packages, seller property condition statements, agency relationship disclosures, and a closing day stack of documents that routinely runs 150 to 200 pages. Most buyers sign in under an hour, initialing things they've never read, guided by a closing agent who is legally prohibited from giving them advice.

This is what buying a home looks like now. And most people assume it must be this way because it has to be.

It didn't always.

When Real Estate Was a Local Business

For much of the 20th century, real estate transactions were genuinely community affairs. Agents were local figures who knew the neighborhood, knew the sellers, and often knew the buyers personally. Bankers were local too — savings and loan officers who lived in the same town as the people they were lending to, who had skin in the game in a very direct sense.

The paperwork reflected that trust. A standard purchase agreement in the 1950s or early 1960s was a brief document — a few pages at most — that described the property, named the parties, stated the price, and outlined the closing date. Contingencies existed, but they were negotiated conversationally and captured in plain language. The mortgage note was similarly concise.

Title searches were done by local attorneys who knew the county records intimately. Title insurance barely existed as a mass-market product. In many transactions, a lawyer's opinion on the title was considered sufficient — and usually was.

None of this was naive. It was a system built on relationships, local accountability, and the fact that everyone involved expected to see each other at church on Sunday. The social fabric of the community was its own form of enforcement.

What Broke the System (And Why the Lawyers Moved In)

The shift began in earnest in the 1960s and 1970s, as several forces converged to fundamentally change the nature of real estate transactions.

The first was scale. As suburban development exploded and Americans became more mobile, real estate transactions increasingly happened between strangers — buyers from out of state, developers with no community ties, lenders operating across multiple markets. The handshake economy doesn't work when nobody knows each other.

The second was litigation. As consumer protection law expanded and courts began holding sellers and agents liable for undisclosed defects, the industry responded with disclosure forms. Lots of them. Every lawsuit that resulted in a judgment against a seller for failing to mention a leaky basement or a cracked foundation spawned a new form designed to prevent the next one.

The third was securitization. When mortgages began to be bundled and sold on secondary markets — a process that accelerated dramatically from the 1980s onward — the loans had to conform to standardized documentation requirements set by Fannie Mae, Freddie Mac, and eventually a labyrinth of regulatory bodies. The local banker who knew your father was replaced by an underwriting algorithm that needed every box checked and every form signed.

Each of these changes was individually defensible. Together, they produced a transaction so complex that the average homebuyer has essentially no idea what they're agreeing to.

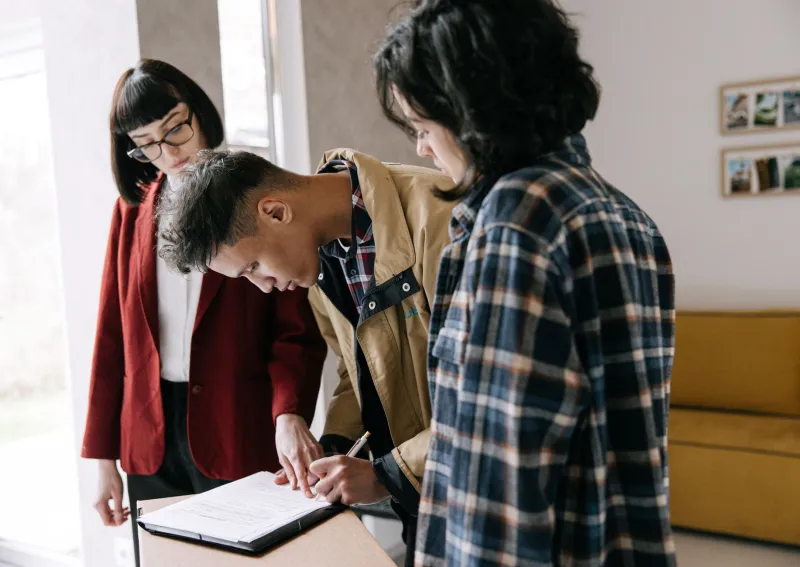

The Closing Table Nobody Understands

Ask anyone who has bought a home in the last decade to describe what they signed at closing. Most will tell you they have no idea. They'll remember the experience — the table covered in paper, the closing agent briskly flipping pages, the slightly panicked feeling that they were agreeing to something they didn't fully understand — but the content itself is largely a blur.

This is not a failure of intelligence or attention. It's a structural problem. The documents are long, written in legal language, and presented under time pressure in a context where the buyer has already committed emotionally and financially. Questioning a document at the closing table feels like stopping a wedding mid-ceremony to read the prenup.

The Closing Disclosure — the standardized form that's supposed to help buyers understand their costs — was itself a reform introduced in 2015 to simplify a previous form that had become incomprehensible. It's better than what it replaced. It's still seven pages long and contains line items that most buyers couldn't explain if asked.

Does the Paper Actually Protect You?

This is the honest question at the center of all of it. And the answer is: sometimes, partially, for some people.

Disclosure requirements have genuinely helped buyers. Knowing that a property is in a flood zone, that the seller is aware of foundation issues, or that the HOA has pending litigation are all legitimately useful pieces of information. The legal framework that requires these disclosures has prevented real harm.

Title insurance, for all its cost, does occasionally pay out — protecting buyers from title defects that would otherwise result in devastating losses.

And the standardization of mortgage documents, while contributing to the paperwork avalanche, has also made it harder for predatory lenders to bury exploitative terms in fine print. Theoretically.

But the system also generates enormous friction and cost without always delivering proportionate protection. Title insurance premiums are paid upfront at closing and primarily benefit the lender's policy, not the buyer's. The buyer's policy is a separate purchase that many people skip because nobody explains it clearly. Closing costs in the U.S. average between 2 and 5 percent of the purchase price — thousands of dollars that go largely to intermediaries processing paperwork.

And for all the documentation, real estate fraud, hidden defects, and predatory lending haven't disappeared. They've just gotten more sophisticated.

The House Still Needs a Roof. The Rest Is Noise.

At its core, buying a home is still what it always was: two people agreeing that a piece of property is worth a certain amount of money, and a lender agreeing to help finance the gap. The fundamental transaction hasn't changed.

What's changed is the ecosystem around it — the attorneys, the title companies, the disclosure coordinators, the escrow platforms, the compliance departments — all of which exist, at least in part, because the system has grown too complex for the people inside it to trust each other without documentation.

Robert's kitchen table deal worked because Robert knew his banker, his agent, and his seller. The modern closing works — to the extent it works — because every party assumes the others can't be trusted without a signed form to prove it.

Maybe that's wisdom. Maybe it's just a very expensive substitute for community.

Either way, the coffee is long cold by the time anyone gets the keys.